Covariance and correlation#

import numpy as np

import matplotlib.pyplot as plt

import math

%matplotlib inline

# Number of points

n =10000

# Generate two uncorrelated gaussian distributed datasets

# mu, sigma = 0, 1

# x = np.random.normal(mu,sigma, n)

# y = np.random.normal(mu,sigma, n)

# # Generate two correlated gaussian distributed datasets

# mu, sigma = 0, 1

# x = np.random.normal(mu,sigma, n)

# y = np.random.normal(x, sigma, n)

# # Generate two anti-correlated gaussian distributed datasets

# mu, sigma = 0, 1

# x = np.random.normal(mu,sigma, n)

# y = np.random.normal(-x, sigma, n)

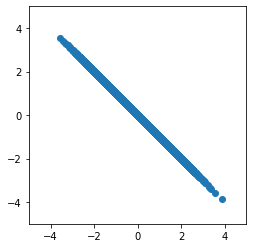

# Generate two strongly correlated gaussian distributed datasets

mu, sigma = 0, 1

x = np.random.normal(mu,sigma, n)

y = np.random.normal(-x,0.0001, n)

# plot them

plt.axes().set_aspect('equal')

plt.axis((-5,5,-5,5))

p = plt.scatter(x,y)

Compute the covariance matrix#

# paste the two arrays into a panda dataset

import pandas as pd

data = pd.DataFrame(dict(x=x, y=y))

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

Cell In[3], line 2

1 # paste the two arrays into a panda dataset

----> 2 import pandas as pd

3 data = pd.DataFrame(dict(x=x, y=y))

ModuleNotFoundError: No module named 'pandas'

# compute the covariance matrix

print(data.cov())

x y

x 0.996748 -0.996749

y -0.996749 0.996750

# the elements on the diagonal are the variances of the datasets x and y

print(data.var())

x 0.996748

y 0.996750

dtype: float64

# the off diagonal element(s) quantify the dependence between x and y

# the covariance matrix is symmetric

Compute the correlation coefficient#

np.corrcoef(x,y)

array([[ 1. , -0.99999999],

[-0.99999999, 1. ]])

# this you can compute by normalizing the covariance to the sqrt of the variances

CovXY = data.cov()

Varx = data.var()[0]

Vary = data.var()[1]

print(f"Correlation = {CovXY.iloc[0,1]/math.sqrt(Varx * Vary)}")

Correlation = -0.9999999949905587